Features

Financial Reports & Markets

Packaging

Report: Specialty papers market to grow from packaging segment

August 19, 2019 By Smithers Pira

Photo: Smithers Pira

Photo: Smithers Pira Flexible packaging, the largest segment within the global specialty papers industry, will maintain a strong growth among all subcategories in the global specialty papers industry as the highly fragmented customer base in North America begins to consolidate, and more traditional commodity paper mills are entering the flexible packaging market.

Expected to have a compound annual growth rate (CAGR) of 2.4 per cent in the next five years, flexible packaging will push overall consumption in applications from 4.72 million metric tons to 5.32 million metric tons, according to Smithers Pira’s new market report, “The Future of Specialty Papers to 2024.”

The global market for specialty papers is projected at 25.03 million tonnes in 2019, out of a worldwide total production of paper and paperboard estimated at more than 450 million tonnes. Demand for specialties is forecasted to reach 28.02 million tonnes in 2024. This represents a CAGR of 2.3 per cent over the five-year period from 2019 to 2024.

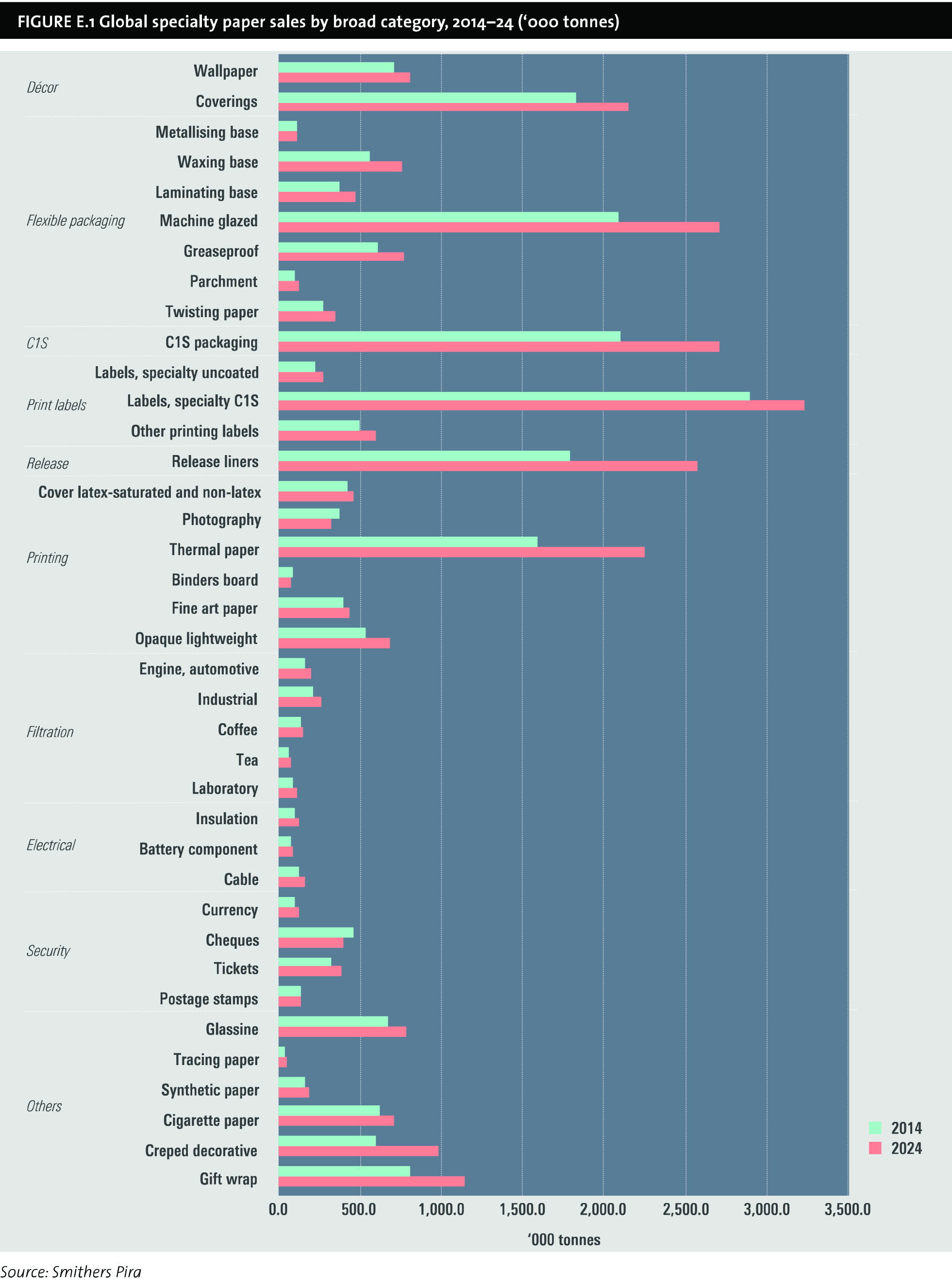

Specialty paper grades fall into 10 broad classifications: decor (including wallpapers and coverings), flexible packaging (including lightweight food papers), C1S packaging (retail and food containerboard), printing labels (self-adhesive and gummed labelstock), release liners, specialty printing (including direct thermal), filtration (automotive, industrial, coffee, tea), electrical, security (including check papers and postage stamps) and a catch-all category simply titled “others” (including cigarette paper and gift wrap).

Global specialty paper sales by broad category

Regional trends

Among the classifications, C1S packaging is the largest and fastest-growing market in the Asia-Pacific region, predominantly in China and India, and it will be critical in pushing total global demand to 2.71 million metric tons by 2024, projecting a 2.7 per cent CAGR across the five-year period.

The Asia-Pacific region will also experience the strongest expansion of sales volume, (a projected 3.8 per cent annual growth), which already consumes the largest tonnage worldwide. China and India are particularly robust. Flexible packaging papers, C1S packaging, printing labels, specialty printing papers and release liners are the largest segments within the global industry.

Market consolidation

Most major categories of specialty papers will grow across 2019–24, but at different rates. While we can expect impressive growth in flexible packaging, security papers will continue to decline in many developed countries, particularly banknotes and cheque papers; as electronic payments, credit cards and email communications continue to shift consumer preferences away from physical paper media.

As the global printing and writing paper industry contracts, specialty paper grades, along with tissue and packaging, are the current engines for growth in the pulp and paper industry. Some traditional specialty sectors, however, are in decline in many regions. These include postage stamps and photographic-base papers.

For more information on “The Future of Specialty Papers to 2024,” visit Smithers Pira.

Print this page